Clint Van Marrewijk

April 8, 2026

A transaction-based framework for valuing pre-feasibility brine projects in the Lithium Triangle.

Lithium brine assets are genuinely hard to value.

Particularly those sitting between maiden resource and feasibility, where there’s no earnings multiple. No DCF you can really trust. No revenue.

So how do you anchor a number?

Start with what’s actually traded

Over the past eight years, let’s sample 16 brine asset transactions in the Lithium Triangle that have been completed.

Those that have both a published transaction value and a compliant resource estimate at the time of the deal.

Divide the enterprise value paid for the total resource in each deal, and you get a key metric: dollars per tonne of LCE in the ground

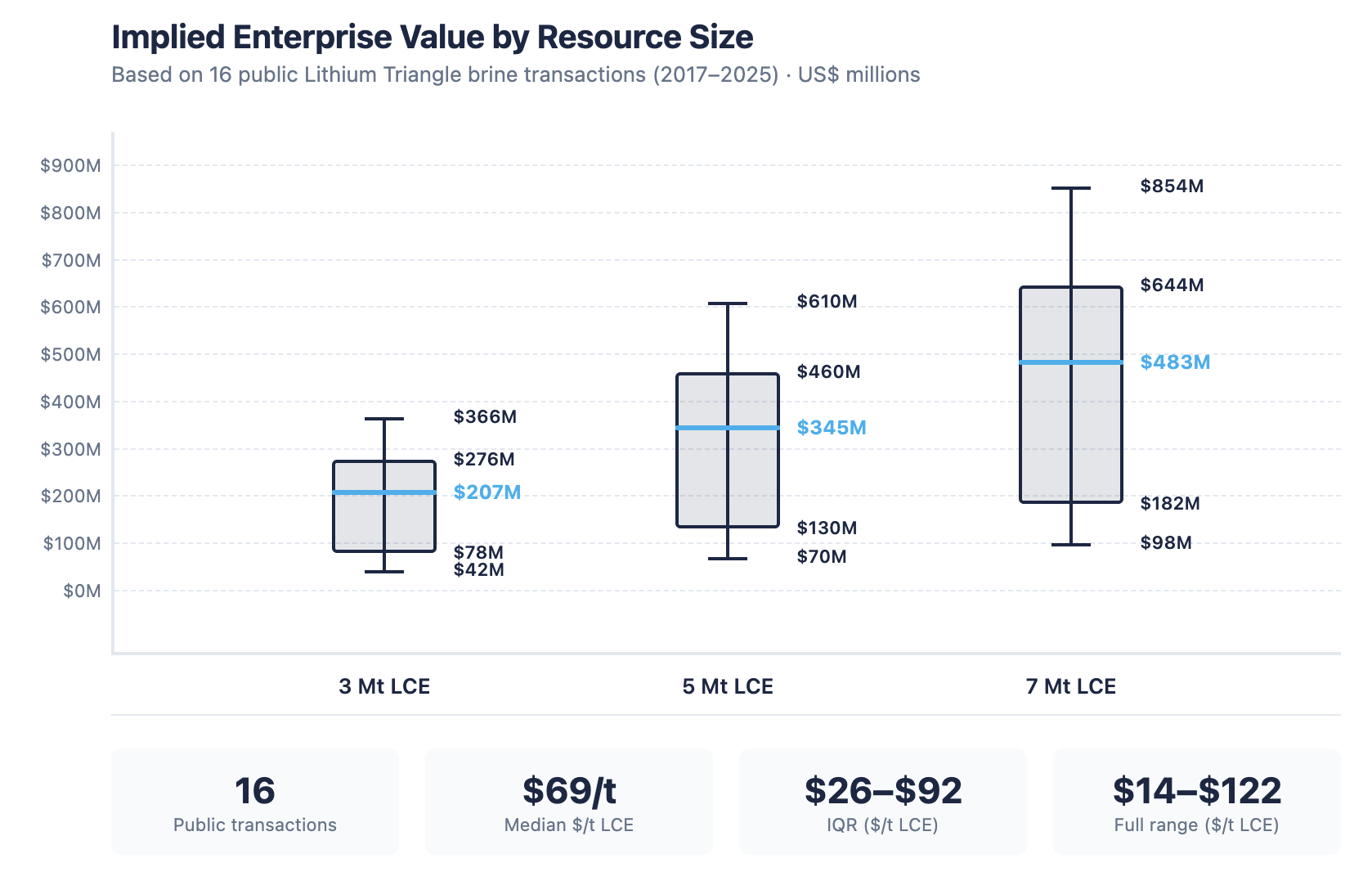

Across those 16 deals the median is US$69/t LCE, with an interquartile range of $26–$92/t.

The bottom quartile tends to be dominated by early-stage assets or distressed sellers.

The top quartile reflects either good-timing, or a good project, or both.

This median price then, is a defensible single-point estimate for a pre-feasibility study brine asset with a credible resource.

- To revisit the 11 key attributes that matter for lithium brine project quality, see our previous post here.

The 2.5 million ton question

A $/ton metric only gets you halfway.

The other key question is: how big does a resource need to be to produce?

Size matters: We looked at every brine project in the Lithium Triangle that has reached production. All nine have resources above 2.5 Mt LCE. The smallest being POSCO’s Sal de Oro at 2.8 Mt (working from public data).

In our opinion, the rule of thumb is clear: 2.5 million tonnes of LCE is where a brine project transitions from an “interesting asset” to a “potential standalone producer.”

Below that size, and there should be a discount applied to the price per tonne in the ground.

Putting it together

- A 3 Mt resource at the median price implies: $207 million.

- A 5 Mt resource: $344 million.

- A 7 Mt resource: $481 million.

These are anchored to what buyers have actually paid, through the highs and lows, of the lithium price cycle.

In theory the spread inside the quartile ranges above, would be impacted by the variables that matter: lithium grade, impurities, project stage, infrastructure, water access, etc.

For example a project at 800 mg/L with road access should sit in the upper quartile. A project at 200 mg/L on a remote salar, with no water rights, should sit in the lower quartile...

That is what you would expect. But there are transactions that are outliers.

The bottom line

Sixteen potential producers. A $69/t median value.

Target a resource above 2.5 Mt if you want to talk about standalone production. Or be willing to accept a discount.

The hard part of course, is getting the geology and flowsheet right…

But that’s a different post.

About Zelandez: Zelandez is a lithium brine services firm with operations across Argentina, Chile, Bolivia the United States and Canada. The team combines subsurface and aboveground expertise: hydrogeology, process engineering, and project economics, to support lithium brine miners. The transaction comps and brine data referenced in this post are drawn from Zelandez's database of 267 tracked projects globally.

Recent Posts

Lithium Brine 101: How to compare and value lithium brine deposits

Using Digital Twin Technology in the Lithium Brine Industry

How the Inflation Reduction Act and US Trade Policy Could Handicap Its Ability to Harness Argentine Lithium Supply

The Lithium Brine Industry Must Share Reinjection Best Practices

Visions of Union County: What Groundwater Management Means for DLE & Lithium Brine Mining in the US